Following article is just a re-collection as I struggle through my thoughts. Not an encouragement of what you should do or not. There is a lot of dynamics and risks on my actions and likely not suitable for anyone who attempt to follow as always.

----------------------------------------------------------------------------------------------------------------------------------

Has been quite some time since I last posted about my trading activities. Maybe is good time to re-collect on it on those that I can remember and correctly remembered. Since the last scare on stable Reits, I have decided to take profit on a number of my higher profit counters.

However, there's still a need to continue my dividend "Story line". This few months saw a number of Reits actions. Very happening months and trading costs have been escalating which I have to watch closely as expense ratio can climb very fast with lowering profits when the market turns while I am searching for the Nirvana Portfolio to suit myself.

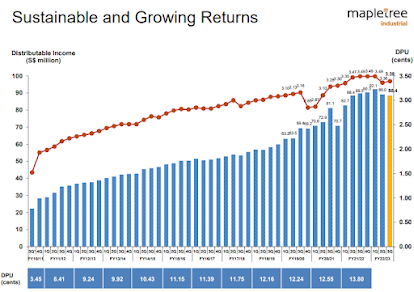

Maple Ind Tr

Not bad for a stock which I started investing only last year. In Year 2018, after dividends is only kopi money. Hardly cover my transaction costs. However the logic is clear for me and which I continue to add even more after. Year 2019 profits kind of exploded. Is good to have a happy closure on this counter.

Basically I cleared out this counter. Good 5 digits profits for Year 2019. Rationale is that it has hit below 5% yield. I do like this counter though as I am expecting DPU growth for some period of time.What this mean is I am no longer have any Maple counters ( sigh ).... . Not sure is the best thing to do but it has been decided and so a counter less.

Ascendas Reit

To cut the the long story short, sold all my Rights Shares however bought the Mother-Shares later. This push my holding relatively high. I have yet completely recovered to my previous max profits on this counter net net. However, at roughly 5.5% yield I am happy to wait while collecting dividends.

This is the largest Reit in town. I have been harping how attractive it is for myself. And I am willing to go along with it growth along Singapore Story Line with the added twist on recent US acquisitions. Certainly I put a lot of faith in the management. I could be wrong and pay for it.

Accordia Golf Trust

AGT is something I owned few years back/ Not so profitable exercise. In fact net net a slight loss if my memory serves me correct. I hate the pendulum swing in the stock prices. The DPU swings too with the directional of the "weather" or weather ...

Back on this counter due to recent news on potential sales of all it's golf courses. The reason I go in is 2 folds. First the NAV and possible premium. Apparently, the market did not drives it high enough so I decided to do a calculated risk to buy some despite the premium. Of-course this is speculation move and can becomes long term holding which isn't that bad with roughly 7% yield @0.675. Yes, high can go higher ... . The fall can be great too sadly.

Fact check on myself. Without AK affirmation, I wouldn't have go in. After keying in the lots acquired on how much dividends I could get, Year 2020 dividends moved up nicely. So I thought maybe I should get 10 lots more but the price has ran away in the seconds that I was deliberating. I always remind myself that when one buy on speculation please treat the trade as such. I did not on this one.

Netlink BNB Trust

Decided to increase my holding since I am not going to clear them all. This to me is a defensive play while yield is average. There's talk about sustainability of the distribution but I am not sure is a concern considering the gearing is low. Anyway the size is risk adjusted and does help to spread out my dividend play. 5G risk is unknown 😱. Something I have to stomach with. However, I got a good enough 5 digits buffers on this year alone.

The history on this one with me is boring. There aren't much profits on this one and for a period of time looking at how shipping trust or harbor trust go, this aren't one of my pillow that I can sleep soundly. I even lose money on this last year after dividends. Other than being similar to a business trust their commonality ends.

The only calculation I did is yield and that they are here to over stays for years to come. There has been many discussion on their viability. So we walk with our eyes open so blame no one. Just have to stay nimble.

FCOT

Took profits about 40% of it few weeks back. Is another nice 5 digits from this year alone in total considering I only start investing in them in Year 2018 and have the lots doubled in Year 2019. Why the confidence is like the enlightenment I had on it being treated as bond-like in nature. This easily explain why I make my moves on a number of other Reit counters.

Just yesterday there is this merger news. Frankly not sure is good or bad timing for me. It has maintained 2.4 cents for longest time I can remember quarterly. So they know how to make Shareholders happy. Let see what they could come out with. Hopefully I will have a better deal from FLT. The suspend is interesting.

Ascendas-h Trust

This has been with me for past few years. Is small but nimble. When I have it I know what I am going into. I have this tract rather closely quarterly and was quite interested in what they have been doing strategically. Unlike others, I have time to tripled my allocation over the years.

Together with the others, sold about 30% off this counter. This is the largest profit of all the reits I have of this year. You can say is re-balance of the profits 😌. I have nothing against Ascott Reit other than offering me a lower yield than AHT can but it is going to be in a stronger entity. Look forward to my Ascott Shares.

DBS

Continue to increase my holding on this at opportune time. Right now is slightly above 8% of my portfolio holding. So, think I am good on this one. CEO performs much better than the others. He knows what is Shareholder values I feel or my feel. The only risk is the digital banking licenses which I have not much clue on the impact. Gut feel is DBS should weather it through safely.

This counter also acts as a counter-balance on the Reits which are interest rates sensitive so that my portfolio do not swing like a pendulum. That's not saying both won't go lower on a single day though. Having dividend like nature and longevity in the business gives me the confidence.

STI ETF

Sold some off when it hits $3.3 early Nov. This is more of re-balance and improving yield moves as STI seems to hit a new peak. (Link). Should have sold more but hindsight is always 20/20. Future purchase will be to nominee account for long term and lower trading cost structure as a personal reminder. If one has followed my blog, STI has not been performing well for past decade. You can try to put your start point before GFC or after it's recovery and the end point today and see whether this is align to my thoughts. I am in it for long term diversification as a portion in my portfolio. With the yield at 3.x%, I would prefer to time the market on this one.

SPH Reit & CMT

Increased some SPH Reit shares as I view this is a better yield performer than CMT. My view is both their dividends and DPU will be quite defensive. Interestingly, I do bought some more CMT this month when it comes back up in yield. Maybe I should have only one of them in the future. There is always this balance between defensive and better yield fluctuating within my mind. Their combine holdings probably square off with AR in exposure.

Frasers 3.65% Bond

With the cash raised, I took some to buy some bonds. Think roughly 10% max holding now that I would go. Not sure this is the right move come to think of it today. I will have to give further thought on this size. This aren't the problem now as I have cash available for opportunity and Frasers family seems running well.

Aims Apac Reit

Average down at 1.373 and then sold half when it rebounded. This is the current size I am happy to hold and sleep well. One of the "alpha" in the Reit team as it provides 7% yield at today price I think. In term of profits, this year is kopi money. I am happy to keep the remaining as long term holding. This does help my Year 2020 plan.

Overall

After all above, there is still good amount of cash in net sales which will be for opportunity. My only concern is my portfolio has not been as stable as before. In the first 3 quarters of the year. almost always one counter will counteract the other falls quite amazingly. Not so now. Maybe the market has turned less bullish or maybe the counters are not in perfect fit to support each other which means will see lumpiness in P/L. P/L and Div are on-track. (updated for privacy 12/21)

Cory

2019-1129